- Webpages

- Documents

- HDFC Life ClassicAssure PlusInvestment

- HDFC Life ClassicAssure PlusInvestment

- HDFC Life ClassicAssure PlusInvestment

For NRI Customers

(To Buy a Policy)

-

![Contact Image]()

Call (All Days, Local charges apply)

-

![Contact Image]()

Email ID

-

![Contact Image]()

Whatsapp

(If you're our existing customer)

-

![Contact Image]()

Call (Mon-Sat, 10am-9pm IST, Local Charges Apply)

-

![Contact Image]()

Email ID

For Online Policy Purchase

(New and Ongoing Applications)

-

![Contact Image]()

Call (All Days & Toll free)

-

![Contact Image]()

Schedule a call

-

![Contact Image]()

Whatsapp

-

![Contact Image]()

Give missed call to buy a policy

-

![Contact Image]()

Email

Branch Locator

-

![Contact Image]()

Locate a branch

For Existing Customers

(Issued Policy)

-

![Contact Image]()

Whatsapp

-

![Contact Image]()

Call (Mon to Sat, from 10 am to 7 pm, Call charges apply)

-

![Contact Image]()

Email

Fund Performance Check

-

![Contact Image]()

Call (Missed Call)

Income Tax Act of 1961: Sections, Goals, Characteristics, and Clauses

Table of Content

1. What Is the Income Tax Act 1961?

2. Some Important Definitions under the Income Tax Act 1961

3. The Exception to Previous Year

4. Which Income Is Taxable Under the Income Tax Act?

5. Who Is Liable to Pay Income Tax?

6. Chapters of the Income Tax Act 1961

7. Main Objectives of Income Tax Act 1961

8. Scope of the Income Tax Act 1961

9. Features of Income Tax Act 1961

10. Important Sections of the Income Tax Act 1961

12. FAQs on the Income Tax Act 1961

13. Conclusion

Looking forward to filing ITR for the first time? Filing tax returns can be challenging for beginners. You have to learn about the rules and regulations, due dates, filing process and more than a few terminologies. But there’s no need to worry; we have you covered.

In this article, we will deep dive into the Income Tax Act 1961, its important sections, features, various terminologies, clauses, scopes and much more. Read along to get further insights about the same.

What Is the Income Tax Act 1961?

The Income Tax Act is a comprehensive statute which was enacted by the Indian Parliament in 1961 framing the rules and regulations governing income tax in India. It is composed of 298 sections, 23 chapters and various other important provisions governing the various taxation aspects which came into effect on 1st April 1962.

Income tax is a type of direct tax that has to be borne by the taxpayer himself/herself. This tax liability cannot be transferred to another person. It is a progressive system of taxation.

It is the most important source of revenue of the Government. The government needs money to maintain law and order in the country; safeguard the security of the country and promote the welfare of the people. Income tax is one of the most important tools to achieve balanced socio-economic growth.

Some Important Definitions under the Income Tax Act 1961

Here are some of the important definitions under the Income Tax Act:

Income Tax:

Assessee:

Assessment:

Previous Year:

Assessment Year:

Income:

Gross Total Income:

Net Total Income:

After claiming deduction U/s 80C to 80U as per Chapter VIA from Gross Total Income, the balance is called Net Total Income. Where there are no deductions Total Income can be equal to Gross Total Income.

It is the tax imposed by the Central Government, calculated based on the total taxable income of an assessee for the previous year.

A person, who is obligated to pay tax to the government under any provision of the IT Act. An assessee can be someone deemed as such or identified as an assessee by default under the provisions of the Act.

Assessment is the fundamental process of validating the accuracy of income declared by the assessee.

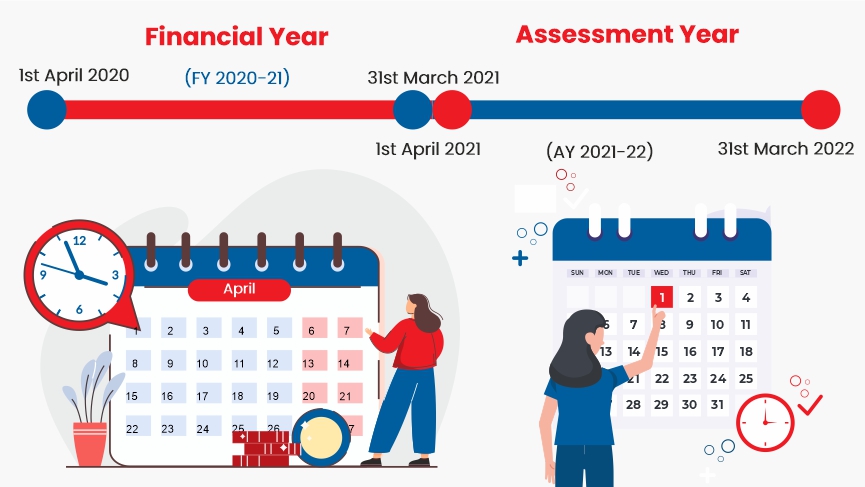

According to the Income Tax Act 1961, the term previous year refers to the financial year which immediately precedes the current assessment year. In simpler terms previous year is the year in which the income is earned. However, in the case of a new business, the previous year will start from the date of incorporation or setting up the profession or business. For a new source of income, the period begins when income is first generated and ends with the given fiscal year.

According to the Income Tax Act 1961, the year in which the income is taxable is known as assessment year. It is the period of twelve months commencing on the first day of April every year and ending on 31st March of the next year.

Income earned in previous year is taxable in the assessment year.

For E.g. for Previous Year 2024-2025, [starting from 1st April 2024 till 31st March 2025]

Assessment Year is 2025-2026 [starting from 1st April 2025 till 31st March 2026]

The definition of income is inclusive but not exhaustive, covering items such as:

- Illegal income received by the assessee

- Any irregular income received

- Taxable income from a foreign source (outside India)

- Any sort of benefit in monetary terms or even non-monetary terms

- All kinds of subsidies, reimbursements, reliefs

- Gifts the ones which are not covered as income izes

- Any kind of casual income, such as gambling on horse races, winnings from lotteries, etc.

Aggregate of various heads of income is called Gross Total Income.

The Exception to Previous Year

Such incomes are taxable as the income of the year just preceding the assessment year at the applicable rates for a taxpayer:

Earnings of a person departing India permanently or for a longer duration

Earnings of non-resident shipping companies lacking a presence or representative in India

Earnings of a person attempting to hand over assets with the aim of evading taxes

Earnings from a discontinued business

Association of persons or body of individuals or artificial juridical person formed for a particular event or purpose

Which Income Is Taxable Under the Income Tax Act?

According to the Income Tax Act, incomes can be segregated under five different heads which are as follows:

Income from salary

Income from house property

Profit and gains from business or profession

Capital gains

Income from other sources

Who Is Liable to Pay Income Tax?

A ‘person’ is liable to pay income tax in India; however, the definition of a ‘person’ under the act is not what we simply understand. The term "Person" has been broadly classified under several categories under Section 2(31), which are as follows:

An Individual

A Hindu Undivided Family (HUF)

A company

A firm

Association of Persons (AOP) or a body of individuals, whether incorporated or not,

A local authority

Every Artificial Juridical Person who has not been covered under any of the above-mentioned categories

Chapters of the Income Tax Act 1961

The Income Tax Act has a total of 23 chapters along with some sub-sections. Listed below are the chapters in the tabular format.

Chapter |

Overview |

Chapter I |

An introduction of the Income Tax Act 1961 and its overview |

Chapter II |

Beginning and scope of the Income Tax Act |

Chapter III |

Income that does not form a part of the total income |

Chapter IV |

Calculation of total income |

Chapter V |

Other income sources forming a part of the assessee’s income, like capital gains, income from properties, businesses and more |

Chapter VI |

Aggregation of income, carry forward and set off of losses |

Chapter VIA |

Deductions applicable to total income computation |

Chapter VIB |

Restriction on specific deductions for companies |

Chapter VII |

Parts of total income not chargeable to income tax |

Chapter VIII |

Applicable rebates and reliefs for calculating income tax |

Chapter IX |

Contains details on double taxation relief |

Chapter X |

Special cases where assessees do not have to pay income tax |

Chapter XA |

General anti-avoidance rules for income tax |

Chapter XI |

Additional tax implications on undistributed profits |

Chapter XII |

Rules of tax calculation in special cases |

Chapter XIIA |

Special rules for certain Non-Resident Indians (NRI) |

Chapter XIIB |

Special tax provisions for certain companies |

Chapter XIIBA |

Special tax provisions for limited liability partnerships |

Chapter XIIBB |

Special tax rules when the Indian branch of a foreign bank gets converted to a subsidiary company |

Chapter XIIBC |

Special tax rules for resident companies in India |

Chapter XIIC |

Special tax rules for retail trade |

Chapter XIID |

Special tax rules for the distributed profits of domestic companies |

Chapter XII DA |

Special tax rules for the distributed income of domestic companies for buying back shares |

Chapter XIIE |

Special tax rules for distributed income |

Chapter XIIEA |

Special tax rules for distributed income by securitisation trusts |

Chapter XIIEB |

Special tax rules for accredited income of specific institutions and trusts |

Chapter XIIF |

Special tax rules for income from venture capital funds and venture capital companies |

Chapter XIIFA |

Special tax rules for business trusts |

Chapter XIIFB |

Special tax rules for income of investment fund schemes and the income received from them |

Chapter XIIG |

Special tax rules for the income of shipping organisations |

Chapter XIIH |

Tax implications on fringe benefits |

Chapter XIII |

Information on Income Tax Authorities |

Chapter XIV |

The procedure of income tax assessment |

Chapter XIVA |

Special rules for avoiding repeated appeals |

Chapter XIVB |

Special rules for assessing search cases |

Chapter XV |

Tax liabilities in special cases |

Chapter XVI |

Special tax rules applicable to firms |

Chapter XVII |

Rules of tax collection and recovery |

Chapter XVIII |

Tax relief on dividend income in specific cases |

Chapter XIX |

Tax refunds |

Chapter XIXA |

Case settlements |

Chapter XIX-AA |

Role of Dispute Resolution Committee in specific cases |

Chapter XIXB |

Advance rulings |

Chapter XX |

Appeals and revision |

Chapter XXA |

Immovable property acquisition in special cases of transfer to prevent tax evasion |

Chapter XXB |

Mode of accepting payments or repayments in special cases in order to counteract tax evasion |

Chapter XXC |

Buying of immovable property by the Central Government in certain transfer cases |

Chapter XXI |

Imposable penalties under the act |

Chapter XXI |

Punishable offences and prosecutions |

Chapter XXIB |

Certificates of tax credit |

Chapter XXIII |

Miscellaneous categories |

Main Objectives of Income Tax Act 1961

Here are some of the primary objectives of the Income Tax Act 1961:

Revenue Generation for Economic development

The primary objective of levying tax is to generate revenue for government so that it carries out the social welfare activities such as building public infrastructure, healthcare, schools, colleges, providing subsidies, defence etc. benefitting the overall development of the society in large.

Ensuring Price Stability:

It aims to establish regulations for direct taxes to maintain price stability in the economy by controlling private spending. It also makes it easy for the government and regulators to control inflation.

Balancing Wealth amongst the Individuals:

India promotes a progressive taxation system, where higher tax rates apply to the wealthy and lower rates apply to comparatively less wealthy individuals. This approach addresses wealth inequality among citizens, aligning with its non-revenue objectives.

Encouraging savings & Investment

The government has provided a wide range of Sections starting from Sec 80C to promote productive investments and save income tax by investing and saving funds. For Example: popular schemes for investment purpose as prescribed by the government are Life Insurance Premium, P.F, National Pension Scheme, Fixed Deposit etc.

Promoting Full Employment:

To promote increased demand for goods and services, the tax regulations have lowered the income tax rates, thereby generating more employment opportunities and contributing to the objective of full employment.

Scope of the Income Tax Act 1961

The scope of income tax you have to pay according to the Income Tax Act 1961 depends on your residential status as shown in the following table.

Type of income |

Residential Status |

||

|

Resident and Ordinarily Resident (ROR) |

Resident but not-Ordinarily Resident(RNOR) |

Non-Resident |

Income received or deemed to be received in India |

Taxable |

Taxable |

Taxable |

Accrued income in India |

Taxable |

Taxable |

Taxable |

Income accrues from outside India, but the profession or business is inside the country. |

Taxable |

Taxable |

Non-taxable |

Income accrues from outside India, but the profession or business is outside the country. |

Taxable |

Non-taxable |

Non-taxable |

The untaxed past foreign income brought into the country. |

Non-taxable |

Non-taxable |

Non-taxable |

Features of Income Tax Act 1961

Listed below are some of the key features of the Income Tax Act of 1961:

Income tax is applicable to income from all sources earned by the taxpayer in the previous year.

Payment of income tax is the responsibility of all taxpayers, and this responsibility is non-transferable to another person.

Income tax is calculated based on the income tax slab applicable to the assessee.

In specific scenarios, tax deductions are subject to a maximum limit per financial year.

It is the Central Government which oversees and controls the system of taxation in India.

The country’s progressive income system ensures that individuals with higher wealth pay higher taxes, contributing more to the welfare of others.

Important Sections of the Income Tax Act 1961

Here are some of the important sections under the Income Tax Act:

Section 80C:

It allows taxpayers to avail a deduction of Rs. 1.5 lakh through Section 80C, Section 80CCC, and Section 80CCD on making investments in specific investment options.

Section 80CCD:

Individual taxpayers can also avail deductions for contributions made to the National Pension Scheme (NPS) or Atal Pension Yojana (APY) under this section and additional deductions over Section 80C.

Section 80D:

For payment of health insurance premiums for themselves, spouses, children, and parents, taxpayers can claim a maximum deduction of Rs. 25,000 (for senior citizens the limit is Rs. 50,000) under this section.

Section 80DD:

Individuals or Hindu Undivided Families (HUF) supporting dependents with disabilities can claim deductions for medical expenses incurred on them.

Sections 80DDB:

For medical expenses incurred for specified illnesses, individuals can claim tax deductions under this section.

Section 80E:

It allows deductions for interest paid on education loans taken for higher education.

Section 80TTA:

It permits Individuals and HUFs to claim a deduction of up to Rs. 10,000 on interest income earned from savings accounts.

Section 80U:

It allows deductions for individuals with mental or physical disabilities or impairments.

Provisions of the Income Tax Act 1961

Here are some of the important provisions of the Income Tax Act.

Filing appeals to the High Court under Section 260A and to the Supreme Court under Section 261

Provision of financial transaction statements and annual information.

Representation by an authorised agent

Determination of income tax liability

Modes for conducting transactions

Authorities are responsible for assessing taxes

Guidelines are provided to subordinate authorities

Schedules to the Act

There are several annexures which have been incorporated and modified within the framework of the IT Act 1961. It aims to cover all the subjects and scenarios which were not addressed in the Act. Over time, several schedules have been included to enhance the comprehensiveness and inclusivity of the IT Act.

FAQs on the Income Tax Act 1961

1. Who introduced the first Income Tax Act in India?

Sir James Wilson, the first finance minister in India introduced the Income Tax Act in 1860.

2. How many sections are there in the Income Tax Act 1961?

The Income Tax Act is composed of a total of 298 sections.

3. What are the main objectives of the Income Tax Act 1961?

The primary objectives of the act are to ensure price stability, reduce balance of payment issues, control cyclical fluctuations, full employment, economic development, etc.

4. What are the components of the Income Tax Act 1961?

The IT Act 1961 has 298 sections, 14 schedules, 23 chapters and various other important provisions governing direct taxation in India.

5. What is Annual Information System?

Annual Information Statement (AIS) is a statement that provides complete information about the prepaid taxes and prescribed financial transactions entered into by taxpayer for a particular financial year.

6. What is Tax Information System?

Taxpayer Information Summary (TIS) is a category-wise summary of tax information available with the Income Tax Department for a particular taxpayer.

7. How to access AIS/TIS?

An assessee can access AIS/TIS information by logging into his income-tax e-filing account or through the mobile app “AIS for Taxpayer”. If he feels that the information furnished in AIS is incorrect, duplicated, or relates to any other person, etc., he can submit his feedback thereon directly from the income-tax e-filing portal, or using an offline utility.

8. What is the difference between e-filing and e-payment?

E-payment is the process of electronic payment of tax (i.e., by net banking or debit/credit card). Whereas, e-filing is the process of electronically furnishing, return of income.

9. How many types of ITR Forms are there?

There are 7 types of ITR Forms available.

Conclusion

Hopefully, by now you have got some clarity on the IT Act 1961, its sections, schedules and chapters. Moreover, you can learn more by downloading the Income Tax Act 1961 PDF directly from the Income Tax Department's official website. Reading this can help you make smarter investments and save a significant amount on taxes.

RELATED ARTICLE

ARN – INT/ED/01/24/8440

Term Plan Articles

Term Plan Articles

Investment Articles

Life Insurance Articles

Tax Articles

Retirement Articles

ULIP Articles

Subscribe to get the latest articles directly in your inbox

Health Plans Articles

Child Plans Articles

Popular Calculators

Francis Rodrigues

Francis Rodrigues

Francis Rodrigues has a decade long experience in the insurance sector, and as SVP, E-Commerce and Digital Marketing, HDFC Life, manages the online sales channel, as well as digital and performance marketing. He has had hands-on experience in setting up sales channels and functional teams from scratch over a career spanning 2 decades.

Vishal Subharwal

Vishal Subharwal

Vishal Subharwal heads the Strategy, Marketing, E-Commerce, Digital Business & Sustainability initiatives at HDFC Life. He is responsible for crafting and ensuring successful implementation of the overall organisation strategy.

Here's all you should know about life insurance.

We help you to make informed insurance decisions for a lifetime.

HDFC Life

Reviewed by Life Insurance Experts

HDFC LIFE IS A TRUSTED LIFE INSURANCE PARTNER

We at HDFC Life are committed to offer innovative products and services that enable individuals live a ‘Life of Pride’. For over two decades we have been providing life insurance plans - protection, pension, savings, investment, annuity and health.

#Tax benefits & exemptions are subject to conditions of the Income Tax Act, 1961 and its provisions.

#Tax Laws are subject to change from time to time.

#Customer is requested to seek tax advice from his Chartered Accountant or personal tax advisor with respect to his personal tax liabilities under the Income-tax law.

Popular Searches

- Term Insurance Calculator

- Investment Plans

- Investment Calculator

- Investment for Beginners

- Best Short Term Investments

- Best Long Term Investments

- 5 year Investment Plan

- savings plan

- ulip plan

- retirement plans

- health plans

- child insurance plans

- group insurance plans

- income tax calculator

- bmi calculator

- compound interest calculator

- income tax slab

- Income Tax Return

- what is term insurance

- Ulip vs SIP

- tax planning for salaried employees

- HRA Calculator

- Annuity From NPS

- Retirement Calculator

- Pension Calculator

- nps vs ppf

- short term investment plans

- safest investment options

- one time investment plans

- types of investments

- best investment options

- best investment options in India

- Term Insurance for Housewife

- Money Back Policy

- 1 Crore Term Insurance

- life Insurance policy

- NPS Calculator

- Savings Calculator

- life Insurance

- Gratuity Calculator

- Zero Cost Term Insurance

- critical illness insurance

- itc claim

- deductions under 80C

- section 80d

- Whole Life Insurance

- benefits of term insurance

- types of life insurance

- types of term insurance

- Benefits of Life Insurance

- Endowment Policy

- Term Insurance for NRI

- Term Insurance for Women

- Term Insurance for Self Employed

- term life insurance plan